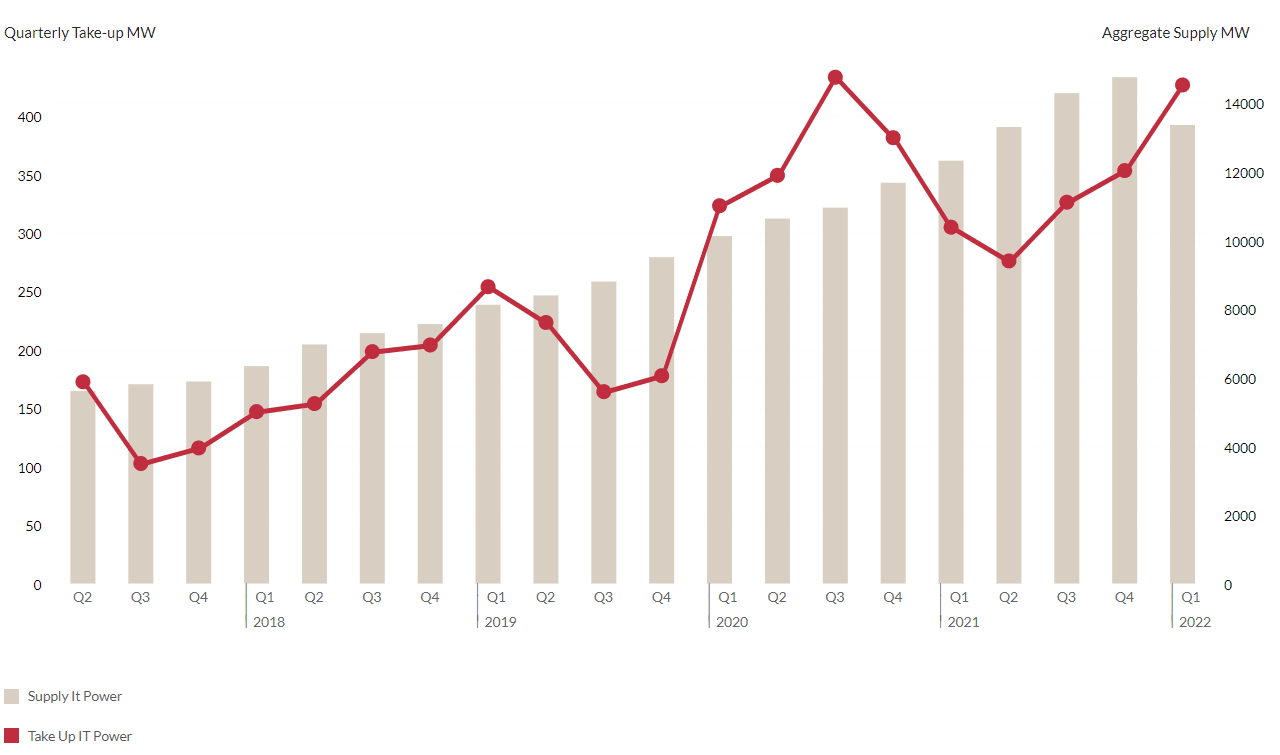

Fuelled by strong market fundamentals, the data center capacity in the APAC region grew by 488MW to total over 8,700MW, says the Knight Frank report on data centers for Q1 2022. Most of this additional capacity comes from the new announcements in Tokyo, Sydney, and Seoul. According to the report, 203MW of capacity was absorbed in Q1 2022 mainly due to public cloud activity, which is significantly higher than the average 127MW per quarter as observed in 2021.

APAC supply and take up IT power

Tokyo, Sydney, and Seoul leading the data center growth in APAC

Tokyo showcased the maximum growth in supply in Q1 2022 from AirTrunk, Colt, and Stack Infrastructure. Multiple assets acquired by Gaw Capital, ESR Cayman, and local asset management company Hulic, are planned for redevelopment into data centers. This is expected to add a capacity of approximately 63MW between them. The growth in IT power supply was accompanied by an above-trend take-up, which is equal to almost three-fourths of the total capacity absorbed in Tokyo in 2021.

Sydney crossed the gigawatt threshold by slightly over 1 gigawatt by adding 144MW of capacity. It was a busy quarter for the data center market in Sydney with the ground-breaking of several facilities including Microsoft’s self-build and Macquairie’s IC3 Super West while other data centers near completion. AirTrunk recorded 85MW take-up in Q1 2022 with the deployment of 30MW capacity at SYD2 and is comparable to the total take-up across the entire year of 2021 in the market.

Alibaba launched its first Availability Zone in Seoul in February. The market had seen the biggest growth in supply over the last 3 years in Q2 2021. This quarter too, the aggregate supply grew by almost a similar amount as in Q2 2021. Facilities being jointly developed by international operators together with asset management companies entering the market boosted the aggregate supply by 136MW. IT power take-up was also higher in Q1 2022 compared to previous quarters due to Digital Realty’s 12MW facility, ICN10, that started operation in January.

Contrary to the above developments, there has not been much activity in the Singapore data center market due to the imposition of the moratorium on data center developments in 2019. This, however, is expected to change soon as the pilot call for applications will be launched in the next quarter. The Hong Kong market too looked dull due to strict COVID measures.

However, the main centers of the APAC region continue to show resilience and adaptability. As markets move towards a ‘living’ with Covid standpoint, the demand drivers strengthen leading to a generally positive trend.

Ben Stirk, Co-Head, Global Data Centres at Knight Frank, said, “Despite significant headwinds – the legacy of Covid, geopolitical turmoil and rising inflation – the Asia-Pacific region continues to register strong data centre growth. The fundamentals support this trajectory, with Asia being the most populous continent and a region where digital transformation is accelerating at pace. There is tremendous hyperscale growth potential underpinned by domestic demand. This, combined with the continued reopening of economies and the loosening of restrictive regulation means further above-trend growth can be expected moving forward.”

Image and source credits: The Knight Frank report

Read next: Edge data centers worldwide to proliferate rapidly in 2-3 years, finds Uptime